Which income turns on first?

CPP, OAS, pensions, RRIF/RRSP, TFSA, taxable accounts, and cash reserves all have different jobs.

Coordinate CPP, OAS, pensions, RRIF/RRSP withdrawals, TFSA strategy, taxable accounts, tax records, insurance, estate questions, and advisor-fit decisions before retirement income starts moving.

The hard part is not one account or one benefit. It is the order of income, tax, investment, document, and estate decisions.

CPP, OAS, pensions, RRIF/RRSP, TFSA, taxable accounts, and cash reserves all have different jobs.

Withdrawals, capital gains, OAS recovery tax, withholding, and missing records can change the plan.

Risk, income need, cash reserve, account role, and advisor service all matter more near retirement.

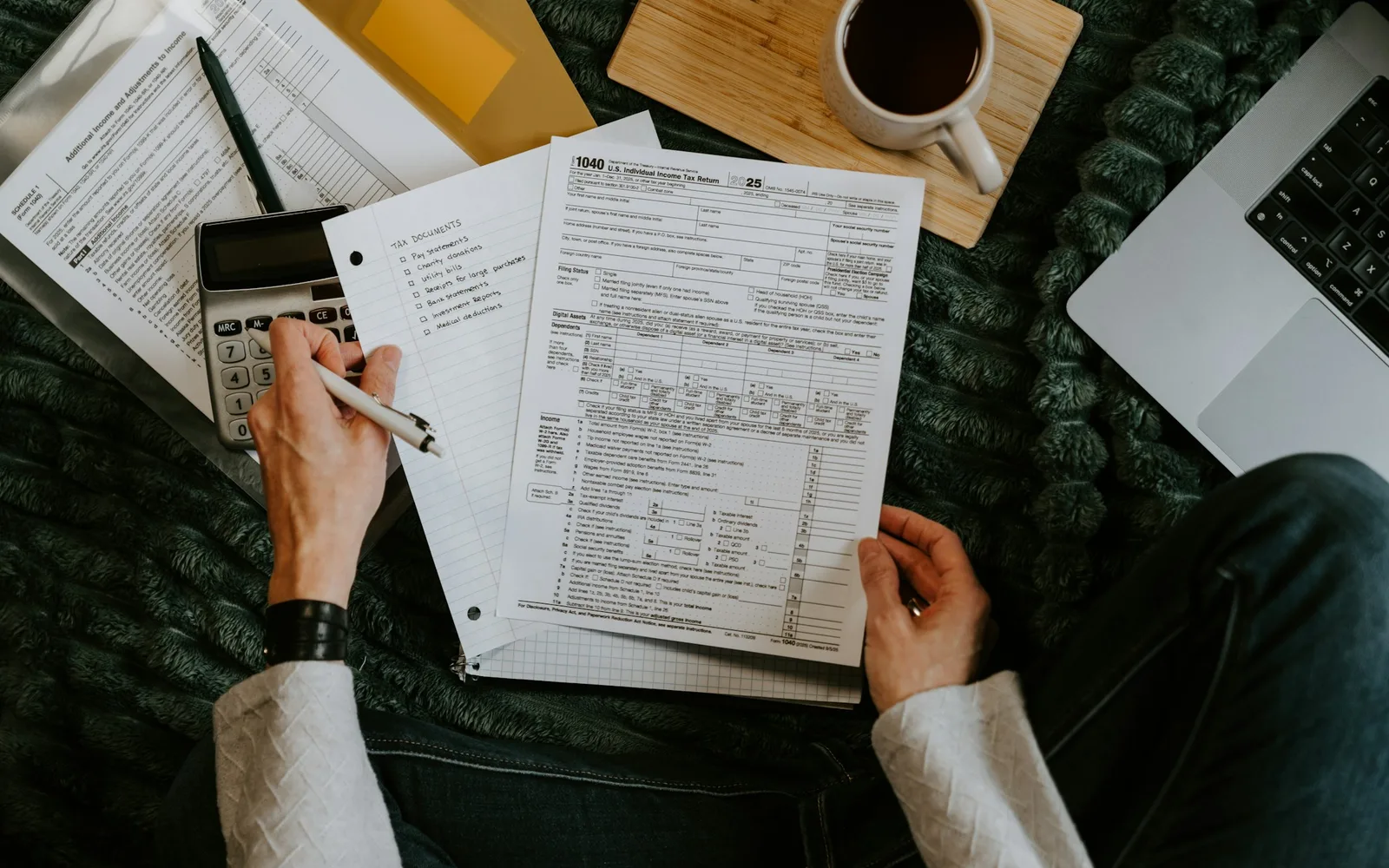

Statements, benefit estimates, tax returns, insurance summaries, and estate notes create the first picture.

Send your name, email, and a short note. The office can route the next step without asking you to send sensitive documents through the website.

The first conversation should reduce pressure. Start with the records, confirm what matters, and leave with a practical next step.

Benefit estimates, pension details, statements, tax returns, insurance summaries, and estate notes.

Confirm whether retirement income planning is the right first conversation before choosing CPP/OAS dates or withdrawal order.

Name the income order, document needs, advisor questions, professional follow-ups, and next three actions.

Stiller Financial starts by making the income, tax, account, document, insurance, estate, and advisor-fit pieces visible before a product, transfer, or paperwork decision takes over.

CPP, OAS, pensions, RRSP/RRIF, TFSA, taxable accounts, and cash reserves are reviewed as one income system.

Withdrawal timing, capital gains, tax slips, withholding, pension income, and OAS recovery tax stay visible.

The first output is a retirement readiness summary, income-source map, document list, and next three actions.

Review CPP, OAS, RRIF/RRSP, TFSA, pensions, taxable accounts, and withdrawal-order decisions.

Read guides

Separate advisor fit, fees, service, tax records, portfolio purpose, and transfer friction before moving accounts.

Open scorecard

Prepare the tax records and secure-route questions that often affect retirement income decisions.

View checklistSend your name, email, and a short note. The office can route the next step without asking you to send sensitive documents through the website.